This piece is authored by Chloé Le Coq, CERRE Research Fellow and University Paris Panthéon-Assas (Dept. of Economics & CRED), Daniel Duma, CERRE Research Fellow and Stockholm Environment Institute, Anna Rita Bennato, Associate Professor (Senior Lecturer) in Economics at Loughborough Business School, and Ewa Lazarczyk Carlson, Associate Professor at Reykjavik University Business School.

As Europe accelerates its journey towards net zero, the concept of flexibility in the energy sector emerges as a key element. The recent CERRE report, “Flexibility in the Energy Sector,” delivers an in-depth exploration of this theme, highlighting the multifaceted nature of flexibility and its critical role in building a resilient, decarbonised energy system.

Understanding flexibility

Flexibility refers to the ability of the energy system—including the power grid and gas infrastructure—to manage ups and downs in demand, supply, and grid capacity. It must do so cost-effectively, across timeframes ranging from minutes to seasons, while supporting our shift to a low-carbon future.

Projections indicate that by 2030, flexibility requirements in Europe could double, and by 2050, they might triple. This surge is driven not only by the variability of renewable generation, but also by the electrification of sectors such as heating and transportation.

Technology is here, but that is not the end of the story

Crucially, the technologies that enable flexibility are no longer speculative—they already exist and are in use—some only at the pilot stage, while others are operating at full scale. On the demand side, smart meters, aggregators, and various demand response programs demonstrate how consumption (and prosumer injection) can be adjusted in real time to meet system needs. On the supply side, hydrogen and biogases are being deployed in flexibility-enhancing applications. Storage solutions, particularly batteries, are also maturing rapidly. Yet, achieving broad deployment of these tools remains challenging and costly. Barriers remain, from upfront investment costs, integration hurdles, public acceptance and data protection concerns, making it essential for the policy framework to foster their wider adoption actively.

Regulation is also in place

The good news? Regulation is also in place. At the European Union level, recent legislation and policy documents increasingly acknowledge the importance of flexibility and its enabling mechanisms—demand-side response, energy storage, and distributed energy resources figure prominently throughout these texts.

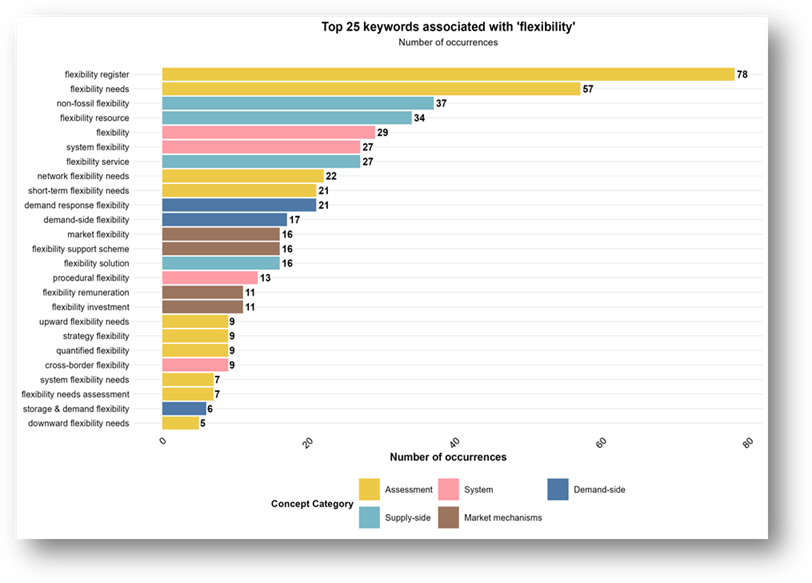

A systematic review of these documents confirms that the discourse still leans toward diagnosing flexibility challenges rather than implementing concrete solutions, as illustrated in the accompanying figure.

Nevertheless, the essential policy instruments are largely in place. Across multiple directives and regulations, the Union either supports or mandates key measures: clearer price signals for consumers (through both retail tariffs and network charges) broader application of market principles (including dedicated flexibility markets), sector coupling between gas/hydrogen and electricity, and recurring assessments of system needs. A network code for demand response is nearing adoption, an integrated electricity-and-gas perspective is required, and digitalisation is being promoted across the entire value chain.

What is missing? Real-world projects show the way forward

Europe is not starting from a blank slate. Pilot programmes and local initiatives across the continent are already testing the solutions on which system flexibility will ultimately depend. In the Nordic countries, dynamic retail tariffs have been deployed at scale, producing observable shifts in consumption. France is advancing the use of biogases, and Germany’s flagship green-hydrogen initiative is exploring the feasibility of flexible electrolysers. Italy and Spain have achieved near-universal smart-meter roll-out, creating the conditions for novel aggregation models. Beyond the EU, California is pioneering vehicle-to-grid integration, Australia is scaling “behind-the-transformer” batteries, and the United Kingdom is developing a harmonised market for flexibility services.

Implementation remains slow and uneven across Member States. Some countries are opening electricity markets to aggregators and other flexibility providers, whereas in others most consumers are on fixed-price contracts.

Each of these examples is a reminder that the building blocks of a flexible energy system already exist. The task now is to replicate, expand, and support them through clearer regulatory guidance.

Learning, aligning, scaling

The path forward is about learning from what already works and making it possible for those solutions to progress more evenly throughout Europe.

Persistent uncertainties and trade-offs must be addressed, including the pace at which hydrogen can be scaled, the commercial viability of carbon capture and storage (CCS), the trajectory of next-generation battery technologies, and the tension between short-term price signals for consumers and long-term investment incentives.

Given these complexities, our recommendations are nuanced. Several proven “quick wins” merit immediate acceleration: digitalisation, battery storage, enhanced interconnections, and more efficient market design. At the same time, further experimentation is essential to clarify the optimal role for less-mature options such as green hydrogen and power-to-X.

Flexibility as the energy transition’s quiet enabler

Europe’s energy future will be cleaner, increasingly electrified, and subject to greater variability. Flexibility may not grab headlines like offshore wind or hydrogen, yet it will be the silent force that keeps the system running smoothly.

The challenge now is to align policy, technology, and market practice to keep up with Europe’s decarbonisation ambitions.

")