This piece is authored by Thomas Le Goff, CERRE Research Fellow and Télécom Paris – Institut Polytechnique de Paris.

The data centre industry is experiencing extraordinary growth across the globe and countries are competing to attract them. Brazil is adopting a special tax regime for data centre services known as “ReData” while South Korea is streamlining permitting. The European Union, of course, is also in the race: for example, Microsoft reportedly plans to invest 10 billion euro to build a data centre in Portugal. This adds to numerous announcements made in 2024 and 2025.

Data centres are critical to Europe’s competitiveness and digital sovereignty. They are essential to productivity-enhancing technologies like cloud computing and artificial intelligence (AI). Yet their impact on energy systems is complex. They are among the most electricity-intensive elements of the digital economy but, at the same time, can help optimise energy and infrastructure use. Our latest work at CERRE showed that, with the right policies in place, data centres can become active contributors to grid flexibility, economic competitiveness, and the EU’s climate and environmental objectives.

Why Do We Need Data Centres on European soil?

Data centres are geostrategic assets. They constitute “final points of control” within the digital value chain. Their location plays an important role in determining who can access, regulate, and potentially disrupt digital services. They are geostrategic assets whose management is deeply intertwined with national and economic security, and European autonomy. Given digital systems underpin critical economic and government functions, dependence on extra-European infrastructure providers, particularly in the cloud and AI sectors, poses risks.

Data Centres also serve EU technological competitiveness goals. The influential Draghi report on EU competitiveness insisted on the need to develop compute infrastructures, stating “the EU is falling behind in providing state-of-the-art infrastructures necessary to enable the digitalisation of the economy”. The European data centre market was valued at $47 billion in 2024 and is projected to reach $97 billion by 2030. In the Netherlands, the data centre and cloud industry is already responsible for 20% of all foreign direct investment and, in Germany, data centres are estimated to have contributed €10.4 billion to GDP in 2024.

Locating Data Centres’ in Europe: National Perspectives

Choosing where to locate a data centre involves technical, economic, environmental, and regulatory factors. Developers must balance the availability of land, access to electricity and the grid, energy costs, cooling conditions, proximity to telecommunications networks and economic hubs, and speed of permitting procedures.

Across the European Union, these variables differ between Member States, leading to uneven patterns of data centre development.

In practice, our study shows that Europe’s most established digital hubs (cities like Dublin, Frankfurt, and Amsterdam) are reaching their physical and electrical limits. Their dense concentration of facilities has created local grid congestion, land scarcity, and growing resistance from local communities. This saturation has prompted regulators and operators alike to reconsider expansion strategies and to explore more geographically diversified approaches.

Northern Europe, by contrast, presents a different profile. Nordic countries offer a cooler climate, abundant renewable generation potential, and well-developed infrastructure, making them natural candidates for energy-efficient and low-carbon data centre operations. However, even there, challenges persist. The pace of developing new generation and transmission capacity is constrained, and increasing electricity demand from both electrification and industrial activity risks tightening the balance between available supply and new loads.

Southern and Eastern Europe bring another set of dynamics. Countries such as Greece see in the data centre industry an opportunity to revitalise industrial regions and accelerate their energy transitions. In Greece, for example, sites formerly dedicated to lignite-based power generation are being converted into “data centre-ready” zones, taking advantage of existing grid connections and industrial land. Yet these regions also face significant environmental stresses, particularly water scarcity, which complicates the deployment of traditional cooling technologies.

France, meanwhile, illustrates how energy system characteristics can become a strategic advantage. The country’s high share of low-carbon, nuclear-based electricity and relatively stable wholesale prices have made it an attractive location for large-scale computing infrastructure. Its interconnected grid further reinforces this comparative strength, although local permitting complexities can offset some of these advantages.

Beyond these national variations, siting decisions increasingly have environmental and social implications. In several regions, media investigations have highlighted the localised impacts of data centre development, including competition for water resources and land use conflicts. These cases underline an important tension: while data centres are indispensable for Europe’s digital sovereignty and competitiveness, their proliferation must be managed to prevent unintended consequences for local ecosystems and communities.

The Way Forward

Europe’s pursuit of digital sovereignty cannot be separated from its quest for energy security and climate neutrality. Otherwise, we risk replacing one dependency with another—swapping reliance on imported gas for dependencies on critical raw materials, foreign software, or extraterritorial AI infrastructure. A sovereign digital transformation requires a coherent framework that integrates energy, environmental, and digital policy objectives.

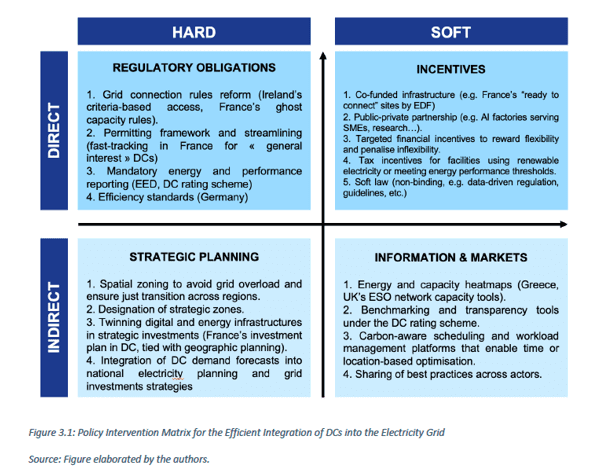

The challenge ahead is to design regulatory and investment environments that ensure data centres strengthen rather than strain Europe’s energy and environmental systems. Policy and regulatory measures across Member States can impose direct or indirect influence, and can use hard (mandatory) or soft (incentive-based or informational) measures. This framework helps map the wide range of instruments available to policymakers, from binding siting and efficiency regulations to fiscal incentives, planning tools, and transparency requirements. Together, these levers can guide private investment in ways that align digital infrastructure deployment with Europe’s energy and climate goals.

What Europe now needs is a smarter, more adaptive policy approach, one that recognises data centres not as passive consumers of electricity, but as active elements of the energy system. Siting decisions should reflect local grid capacity, renewable energy availability, and broader spatial planning considerations, ensuring that new facilities are located where they can best contribute to system resilience. Efficient management of grid connection queues is equally important to free up scarce capacity and avoid unnecessary delays for high-value projects.

At the same time, market access rules must evolve to enable data centres to participate in flexibility and balancing markets. This would allow them to provide valuable services to the grid by shifting workloads, deploying on-site storage, or using waste heat efficiently.

Delivering this vision requires coordination across sectors and borders, blending regulation with market innovation, and aligning energy, industrial, and digital strategies.

For further details on CERRE’s policy recommendations, read our latest report “From Gridlock to Grid Asset: Data Centres for Digital Sovereignty, Energy Resilience, and Competitiveness”.

")